Financial Readiness

Household financial protection during elevated threat conditions at DEFCON 3. Insurance gaps, savings benchmarks, asset protection, and fraud defense based on verified federal data.

Data is sourced from the Federal Reserve SHED survey, Bankrate, FEMA, FTC, and verified financial research. This page provides preparedness information based on current conditions, not investment or insurance advice.

Emergency Savings & Cash Reserves

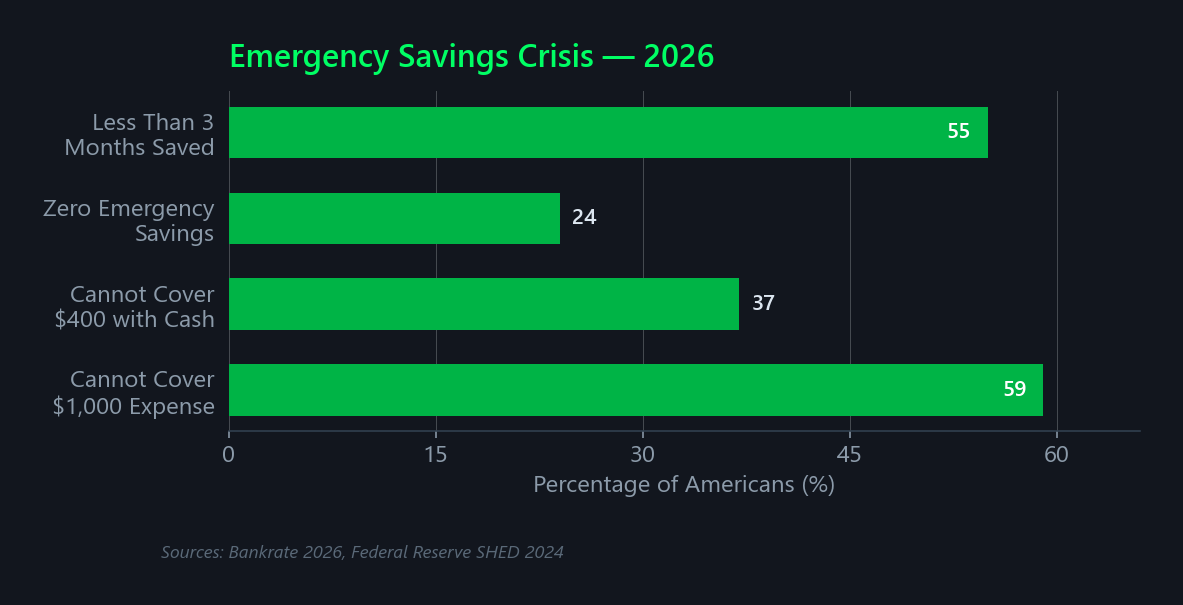

Household financial resilience is under pressure globally. The OECD reports rising cost of living has eroded savings across most member nations, with median household savings rates declining in 23 of 38 countries since 2020. In the United States, Bankrate's 2026 Emergency Savings Report found 53% of Americans cannot cover a $1,000 emergency expense with savings. The median emergency fund balance dropped to $5,000 in 2026 - half the $10,000 reported in 2025. The Federal Reserve's report on the economic well-being of U.S. households in 2025 found 37% of adults could not cover a $400 expense using cash or its equivalent.

Savings Benchmarks

Only 46% of Americans have three or more months of expenses saved. The Federal Reserve's SHED survey found 55% had set aside money for three months of expenses - but the number drops sharply for households under $40,000 annual income. At DEFCON 3, maintaining 30-90 days of liquid reserves is a baseline target. FDIC-insured high-yield savings accounts currently yield 4.5-5.0% APY - a $10,000 emergency fund generates $450-$500 annually in interest while maintaining full federal deposit protection up to $250,000 per depositor per institution.

Cash on Hand

ATM networks and digital payment systems are primary cyberattack targets during elevated threat conditions. CISA has issued advisories for financial sector infrastructure since 2024. Physical cash - enough to cover one to two weeks of essential purchases - provides a fallback when electronic systems are disrupted or bank access is limited. The average American household spends $5,500-$6,200/month on essentials according to BLS data - keeping two weeks of cash on hand means $2,750-$3,100 in physical currency stored securely.

Paycheck-to-Paycheck

51% of Americans report living paycheck to paycheck. 34% - approximately 88 million adults - describe their financial situation as "struggling" or "in crisis." 60% report feeling uncomfortable with their current savings level. Any disruption to income or supply chains compounds quickly without reserves.

When an unexpected expense hits, most American households cannot draw from savings alone. Bankrate's 2026 survey found that only 30% would pay a $1,000 emergency from savings - the rest rely on credit cards, income timing, personal loans, or borrowing from family. Households with no liquid buffer absorb shocks through debt, deferred bills, or foregone necessities.

Insurance Coverage & Protection Gaps

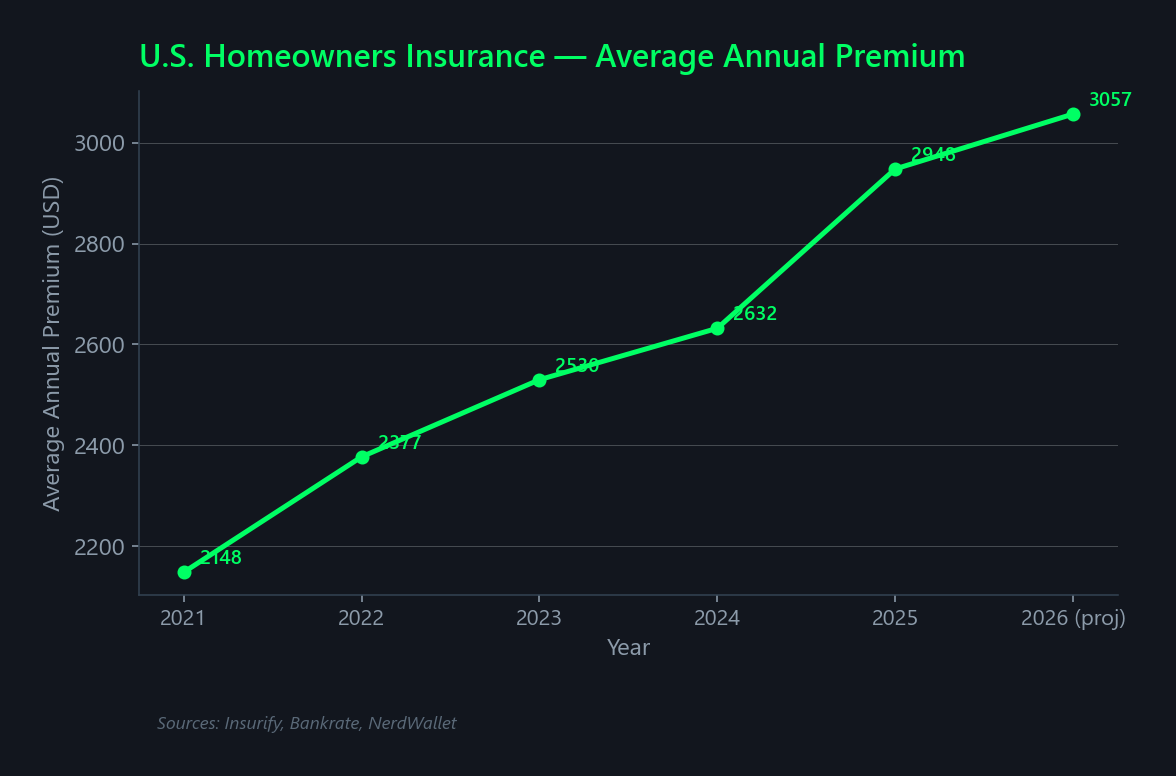

Global insurance premiums are rising as geopolitical instability, natural disasters, and inflation compound risk across all regions. Swiss Re's sigma report estimates global non-life insurance premiums grew 2.6% in real terms in 2025, down from 4.7% in 2024, with emerging markets seeing steeper increases. In the United States, the average homeowner now pays $2,948 annually for home insurance - up 12% in 2025 alone. Insurify projects another 4% increase to $3,057 by the end of 2026. Six states saw premium increases above 20% in 2025, with Minnesota at 34% and Colorado at 33%. Florida remains the most expensive state at approximately $8,300 per year, nearly three times the national average. In Europe, the European Insurance and Occupational Pensions Authority reports property insurance costs rose 8-12% across the EU in 2025, driven by climate-related claims and conflict risk.

Homeowners Coverage

The average homeowner pays $900 more per year than in 2021. Standard policies typically exclude flood, earthquake, and war-related damage. Confirm your policy covers wind, fire, and civil disturbance. FEMA's 2024 survey found 87% of homeowners had insurance but only 43% of renters - leaving millions of households exposed.

Life Insurance Gap

102 million Americans are uninsured or underinsured for life insurance - 75 million without any coverage and 27 million with insufficient coverage. 30% of households would face financial hardship within one month of losing a primary wage earner. 72% of Americans overestimate the cost of basic term life insurance by a factor of three or more.

Coverage Review

Review all policies for conflict-related and terrorism exclusions. Confirm flood, wildfire, and disaster riders are active and coverage limits reflect current replacement costs, not purchase prices. Document all assets with timestamped photos stored off-site or in encrypted cloud storage. Update beneficiary designations annually.

Identity Theft & Financial Fraud Defense

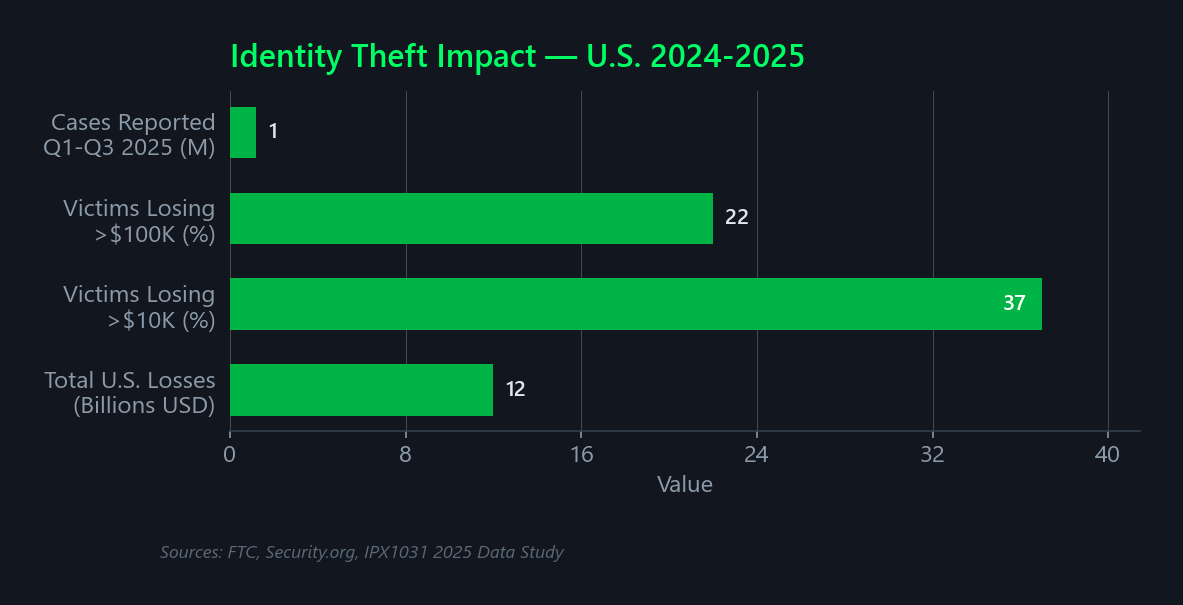

Identity theft and financial fraud are growing worldwide. Nasdaq's 2026 Global Financial Crime Report put global fraud scam and bank fraud losses at $579 billion in 2025, with digital fraud increasing across every region. In the United States, the FTC reported $15.9 billion in consumer fraud losses in 2025, up from $12.5 billion in 2024, across roughly 3 million reports. Identity theft reports filed from January through September 2025 already exceeded the full-year 2024 total, the agency said. The Identity Theft Resource Center found 37% of identity crime victims lost $10,000 or more, with 22% reporting losses above $100,000. European fraud losses are also rising, with the European Central Bank reporting a 15% increase in unauthorized payment transactions across the eurozone in 2024.

Credit Monitoring

Freeze credit with all three bureaus (Equifax, Experian, TransUnion) - free under federal law. Set up fraud alerts and monitor account activity weekly. Nearly 60% of U.S. businesses reported higher fraud losses in 2025, driven by increasingly sophisticated attacks that often target consumer data as a secondary effect. Paid credit monitoring services ($10-$35/month) add real-time alerts, dark web scanning, and identity theft insurance with coverage up to $1 million in fraud losses - a cost many financial planners consider justified during elevated threat periods.

Digital Security

Use unique passwords for every financial account with a password manager. Enable two-factor authentication on all banking, investment, and insurance portals. Iran-linked groups have specifically targeted financial sector networks in 2025-2026, according to CISA advisories for the financial sector.

Document Protection

Store Social Security cards, passports, birth certificates, and financial records in fireproof safes with copies in a secure off-site location. Shred all financial documents before disposal. The FTC reports that tax-related identity theft and government benefits fraud remain the fastest-growing categories of identity crime.

Estate Planning & Legal Preparedness

Estate planning gaps are a global vulnerability. In the UK, approximately 54% of adults do not have a will. Australia reports similar rates, with over 50% of adults lacking basic estate documents. In the United States, only 24% have a will in 2025 - down from 33% in 2022, according to Caring.com's annual survey. 55% have no estate plan of any kind. Among adults 25-54, just 27% have a will. The top reason for delay: 43% say they "just haven't gotten around to it."

Essential Documents

A basic estate plan includes a will, durable power of attorney, healthcare directive, and beneficiary designations on all financial accounts. Without a will, state intestacy laws determine asset distribution - which may not reflect your wishes. 56% of Americans believe they do not have enough assets to justify an estate plan, but intestacy affects families at every income level. Online estate planning services range from $150-$500 for basic documents, while attorney-drafted plans typically cost $1,000-$3,000 - both far less than the $10,000+ average probate cost for estates without a will.

Emergency Access

Designate a trusted contact who can access critical financial accounts and insurance policies during an emergency. Provide a sealed document package with account numbers, policy numbers, attorney contacts, and digital account credentials. Pew Research found that while 81% of adults over 72 have a will, only 24% of adults 18-34 do - leaving younger families most vulnerable to probate complications.

Annual Review

Review and update estate documents annually or after major life events. Confirm beneficiary designations on retirement accounts, life insurance policies, and payable-on-death bank accounts match current intentions. During elevated threat conditions, having current documents prevents delays in accessing funds, making medical decisions, or managing property.

Household Debt & Inflation Pressure

Global household debt is at record levels. The Institute of International Finance reports total global household debt exceeded $58 trillion in 2025, with advanced economies carrying the highest per-capita burden. In the United States, household debt reached $18.78 trillion at the end of Q4 2025 - a record according to the New York Federal Reserve. Consumer prices remain approximately 29.6% higher than December 2019 according to BLS Consumer Price Index data. Grocery spending has risen sharply, with USDA data showing a typical family of four now spending $300 or more per week on food. European households face similar pressure - eurozone inflation, while moderating, has left cumulative prices 18-22% above 2019 levels across most EU member states. 35% of Americans report feeling trapped in a cycle of debt, and 52% worry daily about their finances.

Debt Reduction

Prioritize high-interest debt - credit card rates averaged over 20% in 2025. Eliminating monthly interest payments frees cash for emergency reserves. The Committee for a Responsible Federal Budget warns that U.S. national debt at 100% of GDP limits the government's ability to respond to the next economic shock, making household-level resilience more critical. Paying off the average U.S. credit card balance of $6,580 at 20.7% APR saves approximately $1,360 annually in interest - money that can be redirected to emergency savings or insurance premiums.

Grocery & Energy Costs

Food prices rose 2.9% in 2025, with a projected 3.1% increase in 2026 according to the USDA Economic Research Service. 82% of consumers modified shopping behavior in 2025, primarily seeking sales and switching to cheaper brands. Gasoline at $4.05/gal according to EIA, up sharply since the Iran conflict began in February 2026.

Crisis Budgeting

During elevated threat conditions, separate essential expenses (housing, food, utilities, insurance, medical) from discretionary spending. Build a 30-day essential-only budget as a fallback plan. Cutting discretionary spending first preserves access to necessities during a prolonged disruption.

Financial Preparedness Checklist

Based on current DEFCON 3 conditions and verified federal guidance, these are priority actions for household financial protection.

Immediate (This Week)

Freeze credit at all three bureaus. Enable two-factor authentication on all financial accounts. Locate and secure essential documents (will, insurance policies, account numbers). Confirm you have at least one week of cash on hand for essential purchases. Review all insurance policies for exclusion clauses.

Short-Term (30 Days)

Build or verify a 30-day essential-only budget. Start or increase automatic transfers to an emergency savings account. Update beneficiary designations on retirement accounts and insurance policies. Create or update a will and healthcare directive. Document all assets with timestamped photos.

Ongoing

Target 90 days of essential expenses in accessible savings. Pay down high-interest debt to free monthly cash flow. Review insurance coverage annually - confirm replacement costs, not purchase prices. Monitor credit reports weekly during elevated threat conditions. Maintain a sealed emergency document package accessible to a trusted contact.